Simple Steps to Build and Protect Your Credit

This understanding credit guide gives you a clear look at how credit works, why it matters, and how you can strengthen your score with simple steps. Credit affects more than loans. It can influence your rent, insurance rates, and even job applications. When you learn how credit works, you gain power over decisions that shape your financial future.

As I add more content to Centsible Future, this guide will grow with examples, checklists, and step-by-step tools.

Understanding Credit Guide: What Credit Really Is

Credit measures how trustworthy you are with borrowed money. Lenders look at your past behavior to decide how risky it is to lend to you now. Although the system can feel confusing at first, it becomes more manageable once you understand the pieces that make up your score.

A strong credit score opens doors. A weak score makes everything more expensive.

Why Your Credit Score Matters

Your credit score affects:

-

Loan approvals

-

Interest rates

-

Apartment applications

-

Car insurance rates

-

Cell phone plans

-

Security deposits

Even if you prefer not to borrow money, your score can still impact major life decisions. Because of that, learning how credit works gives you an advantage many adults never receive.

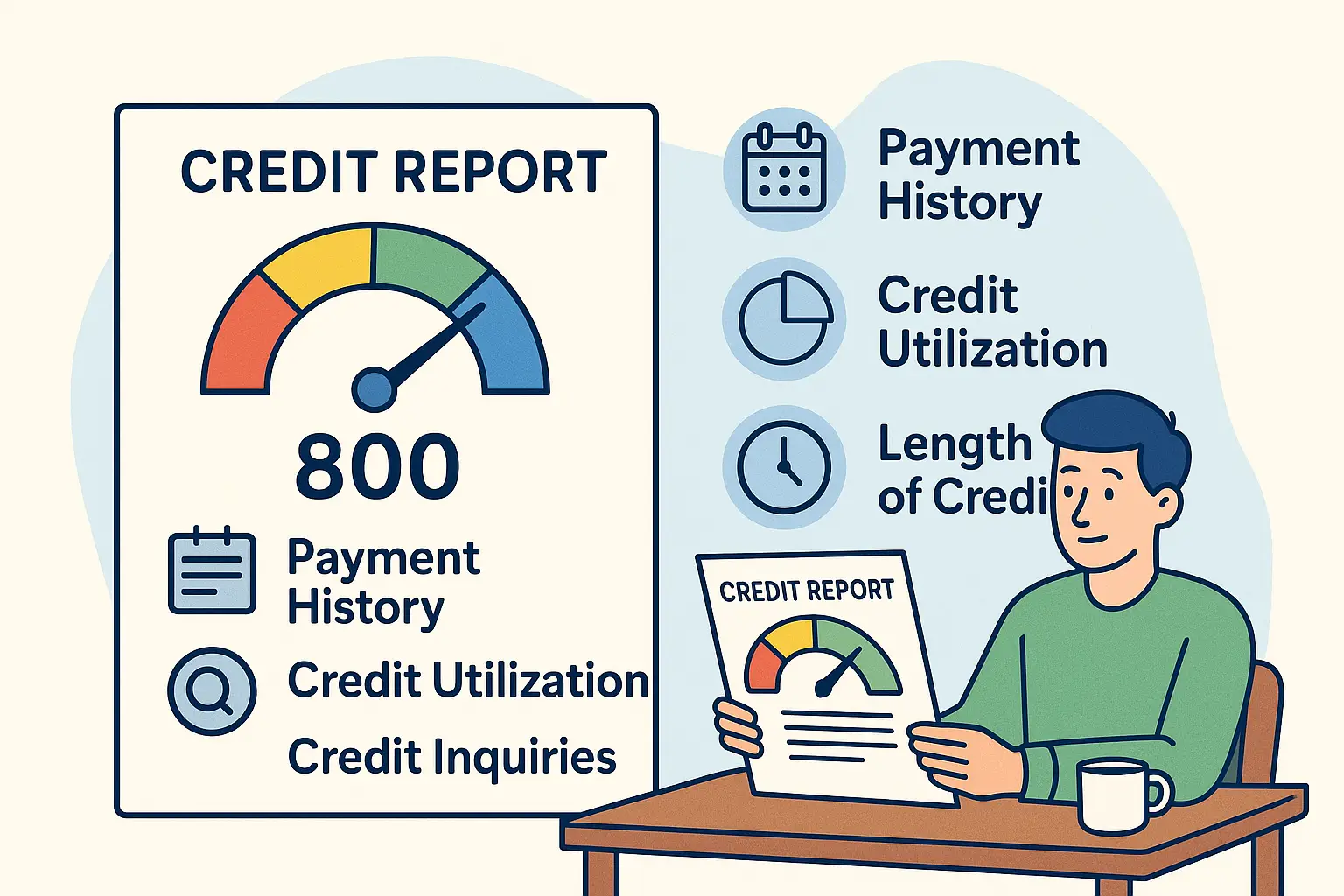

The Five Factors That Make Up Your Credit Score

Most scoring models use the same five categories. When you understand them, improving your score feels much easier.

1. Payment History (most important)

This shows whether you pay bills on time. Even one late payment can drop your score, but consistent on-time payments build trust fast.

2. Credit Utilization

This is the percentage of available credit you’re currently using. Lower is better. Staying under 30 percent is a helpful general guideline, though lower numbers improve your score even more.

3. Age of Credit Accounts

Older accounts help your score because they show stability. Keeping long-standing accounts open—especially ones in good standing—helps you build a stronger history.

4. Credit Mix

Having different types of accounts (credit cards, car loans, student loans, etc.) shows lenders you can handle multiple responsibilities. You don’t need every type, but a mix helps.

5. New Credit Inquiries

Each time you apply for new credit, a hard inquiry appears on your report. A few inquiries are normal. Too many can suggest risk.

How to Check Your Credit Report for Free

You can review your credit report at AnnualCreditReport.com, the only website authorized by federal law.

This allows you to spot:

-

Errors

-

Identity theft

-

Old accounts

-

Incorrect balances

-

Outdated information

Reviewing your report is one of the easiest ways to protect yourself.

How to Build Credit From Scratch

If you’re new to credit or your score needs a reset, you can start with simple steps.

1. Use a Secured Credit Card

You place a deposit, and that deposit becomes your credit limit. Because the risk is low for the lender, these cards help you build credit safely.

2. Become an Authorized User

A family member with good credit can add you to their card. As long as they pay on time, your score benefits too. This is one of the fastest ways to jump-start your history.

3. Pay Small Bills With Your Card

Use your card for predictable expenses like gas or groceries. Then pay it off each month. This builds healthy patterns without adding stress.

4. Keep Your Utilization Low

Even if you have a high limit, avoid carrying balances that are too large. Because high utilization lowers your score, keeping it low protects your progress.

How to Fix Your Credit If It’s Low

You can repair credit over time using simple habits.

1. Pay on Time—Every Time

Payment history has the biggest impact. Even one consistent month at a time makes a difference.

2. Lower Your Credit Utilization

Paying down balances or asking for a credit limit increase can improve this category quickly.

3. Dispute Errors

Many reports contain mistakes. Fixing incorrect information can raise your score without paying anything.

4. Avoid Opening Too Many Accounts

New inquiries can pull your score down temporarily. Because of this, space out applications when possible.

What Hurts Your Credit Without You Realizing It

Several everyday habits can hurt your score even if you don’t notice them happening:

-

Letting balances climb every month

-

Closing your oldest credit card

-

Missing payments by accident

-

Applying for several cards at once

-

Ignoring fraud alerts

Fortunately, most of these issues can be corrected with a bit of awareness and a few small adjustments.

How Long It Takes to See Credit Improvement

Improvement depends on your situation, but most people see changes in:

-

30 days for utilization changes

-

1–3 months for consistent on-time payments

-

3–6 months after correcting errors

-

6–12 months after rebuilding from major issues

Credit grows slowly, but it grows steadily when you stick to a plan.

Where to Go Next

If you want to strengthen your money foundation, start with:

Budgeting Basics Guide

To check your credit report safely, visit:

https://www.annualcreditreport.com

This understanding credit guide will expand with templates, examples, and step-by-step strategies to help you build strong, lasting credit.